Economic uncertainty doesn’t eliminate wealth-building opportunities—it reshapes them. History shows that disciplined investors often grow wealth faster during volatile periods by focusing on long-term ownership, diversification, steady cash flow, and emotional discipline. This guide explains how to build wealth even when the economy wobbles, using real-world examples, proven strategies, and practical steps anyone can apply.

Introduction: Why Economic Wobbles Create Opportunity, Not Just Fear

Every generation believes it’s living through unprecedented economic uncertainty. Rising inflation, interest-rate hikes, market volatility, job insecurity, and alarming headlines dominate the news cycle. For many Americans, this creates a sense of paralysis—Should I invest? Should I wait? Should I just protect what I have?

Yet history repeatedly delivers a powerful lesson: economic instability does not destroy wealth—poor financial behavior does.

From the Great Depression to the dot-com crash, the 2008 financial crisis, and the COVID-era shutdowns, wealth has consistently been built during times of uncertainty. The difference between those who thrive and those who struggle isn’t luck or timing—it’s strategy, patience, and emotional discipline.

This article will show you how to build wealth even when the economy feels unstable, without requiring perfect predictions, complex financial instruments, or insider knowledge.

1. Why Economic Wobbles Are Normal—and Not a Signal to Panic

One of the most damaging misconceptions about money is the belief that stable economic growth is the norm and downturns are rare disasters. In reality, economies move in cycles.

Over the past century, the U.S. economy has experienced:

- Multiple recessions

- Inflationary periods

- Market corrections and crashes

- Interest-rate tightening cycles

Despite this, long-term investors who stayed consistent saw their wealth grow significantly over time.

Economic wobbles are not system failures—they are rebalancing events. Prices adjust, inefficient businesses disappear, and opportunities are repriced. Those who understand this view volatility differently than those who don’t.

2. How Wealth Is Actually Built During Uncertain Times

Wealth is rarely built by predicting short-term economic movements. It’s built by positioning yourself to benefit regardless of what happens next.

During uncertain periods, successful wealth builders focus on:

- Ownership instead of speculation

- Time in the market instead of timing the market

- Fundamentals instead of headlines

Consider investors who continued investing during the 2008 crisis. While markets initially declined, those who stayed invested—and kept contributing—benefited enormously during the following recovery.

The key insight is simple but powerful: economic downturns don’t erase value; they temporarily obscure it.

3. Should You Invest When the Economy Feels Unstable?

This is one of the most common and emotionally charged financial questions Americans ask.

The instinct to wait for “clarity” feels logical—but it often backfires. Markets typically recover before the economy feels better. By the time headlines turn positive, much of the opportunity has already passed.

Studies from major investment firms consistently show that investors who remain invested—even during recessions—outperform those who move in and out of the market.

The goal isn’t to invest recklessly, but to invest intentionally and consistently.

4. Why Diversification Becomes Essential When the Economy Wobbles

When markets are rising, concentrated bets can feel rewarding. When uncertainty hits, concentration becomes dangerous.

Diversification is not about eliminating risk—it’s about controlling it.

A resilient wealth-building approach spreads exposure across different asset types that respond differently to economic conditions. When one area struggles, another may stabilize or grow.

A diversified strategy helps:

- Reduce emotional decision-making

- Limit catastrophic losses

- Improve long-term consistency

Diversification doesn’t guarantee profits, but it dramatically improves survival—and survival is the foundation of wealth.

5. The Importance of Cash Flow During Volatile Periods

During economic wobbles, asset values may fluctuate sharply. Cash flow, however, provides stability.

People with steady income-producing assets often experience less stress and greater flexibility during downturns. Cash flow allows you to:

- Cover expenses without selling investments

- Take advantage of discounted opportunities

- Maintain confidence during uncertainty

Even modest recurring income can be a powerful buffer against financial panic.

6. Inflation: The Silent Threat to Long-Term Wealth

Inflation is one of the most misunderstood forces in personal finance. It doesn’t make headlines like market crashes, but over time it quietly erodes purchasing power.

Money that sits idle for too long loses real value. That’s why long-term wealth builders prioritize assets that historically grow faster than inflation.

Owning productive assets—rather than hoarding cash—helps preserve and grow purchasing power over time.

The goal isn’t to avoid inflation completely, but to outpace it.

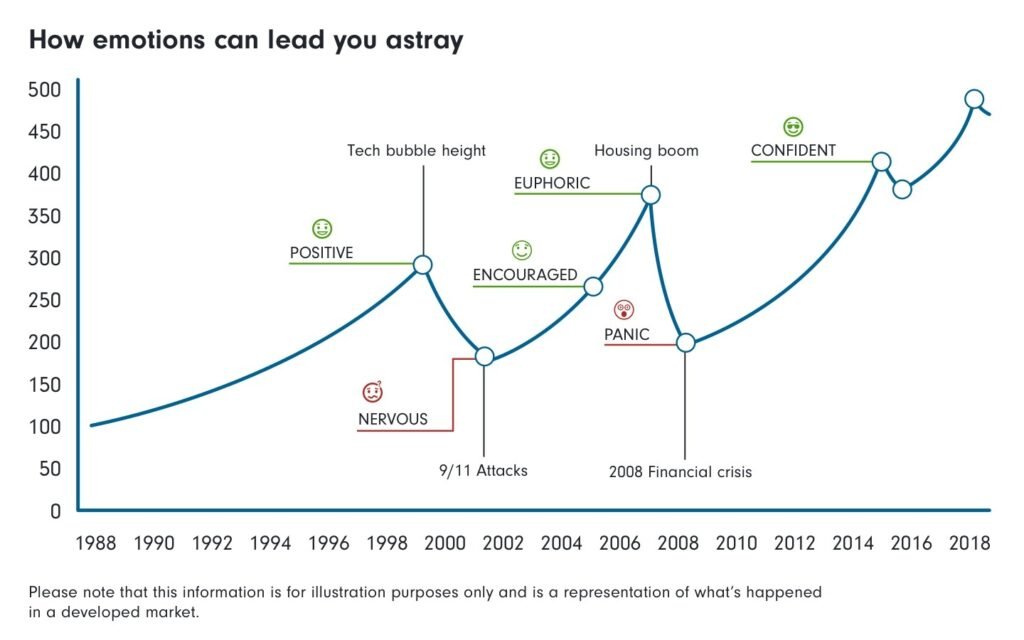

7. Emotional Discipline: The Most Underrated Wealth Skill

Fear and greed drive most poor financial decisions.

During downturns, many people:

- Sell after losses

- Stop investing altogether

- Chase “safe” assets at peak prices

Emotionally disciplined investors behave differently. They rely on plans, not feelings. They understand that volatility is temporary, but bad decisions can be permanent.

Over time, emotional discipline often matters more than intelligence or income when it comes to building wealth.

8. How Dollar-Cost Averaging Works in Your Favor

Dollar-cost averaging—investing a fixed amount regularly regardless of market conditions—is one of the most effective strategies during volatility.

This approach:

- Removes the pressure of timing decisions

- Automatically buys more when prices are low

- Encourages consistency over perfection

Many successful retirement portfolios are built not through brilliant market calls, but through years of steady contributions during both good and bad times.

9. Why Your Skills Are a Financial Asset Too

Wealth isn’t only built through investments. Your ability to earn, adapt, and create value is a powerful form of capital.

During economic uncertainty, people who invest in:

- New skills

- Career flexibility

- Side income streams

often recover faster and emerge stronger when conditions improve.

Financial resilience is about options, and skills create options.

10. Long-Term Thinking Beats Short-Term Prediction Every Time

Trying to forecast short-term economic movements is tempting—but even professionals get it wrong consistently.

What does work is aligning financial decisions with long-term goals and sticking to them through uncertainty.

Investors who focus on:

- Decade-long horizons

- Gradual accumulation

- Ownership of productive assets

tend to succeed regardless of short-term economic noise.

Practical Strategies to Build Wealth When the Economy Wobbles

- Continue investing consistently rather than waiting for perfect conditions

- Maintain diversified exposure instead of concentrated bets

- Keep emergency reserves to avoid forced selling

- Focus on assets that can generate long-term growth or cash flow

- Invest in personal skills and adaptability

Frequently Asked Questions (Trending & SEO-Optimized)

1. Can you really build wealth during a bad economy?

Yes. Many fortunes are built during downturns due to lower asset prices and reduced competition.

2. Should I stop investing during a recession?

Historically, stopping investments often reduces long-term returns more than continuing.

3. What assets perform best during economic uncertainty?

Diversified equities, quality businesses, and long-term investments tend to recover well.

4. How much cash should I hold during volatile times?

Enough for emergencies and flexibility—but not so much that inflation erodes its value.

5. Is investing risky during uncertain markets?

Risk exists, but disciplined, long-term investing has historically been effective.

6. How do I protect my retirement savings during downturns?

Diversification, long-term planning, and avoiding panic-driven decisions are essential.

7. Should beginners invest during economic instability?

Yes—especially through diversified, consistent strategies.

8. How does inflation affect long-term wealth?

Inflation reduces purchasing power, making asset ownership critical.

9. What is the biggest mistake people make during downturns?

Selling in panic and abandoning long-term plans.

10. How long should I stay invested?

Ideally for decades, aligned with long-term financial goals.

Final Thought: Stability Comes From Strategy, Not Conditions

Economic wobbles are inevitable. Financial collapse is not.

The people who build wealth aren’t those who predict the future perfectly—they’re the ones who prepare for uncertainty, stay disciplined, and let time work in their favor.

In the end, resilience—not prediction—is the true engine of wealth.