Global debt has surged past $315 trillion in 2025, setting off alarms that few Americans are hearing. While inflation has eased, a deeper, quieter threat looms — the mounting global debt crisis. This article explores how escalating debt levels in major economies could erode U.S. wealth, impact investments, and reshape the future of financial stability — and what smart investors can do to prepare.

1. Why Is Global Debt Becoming a Growing Concern in 2025?

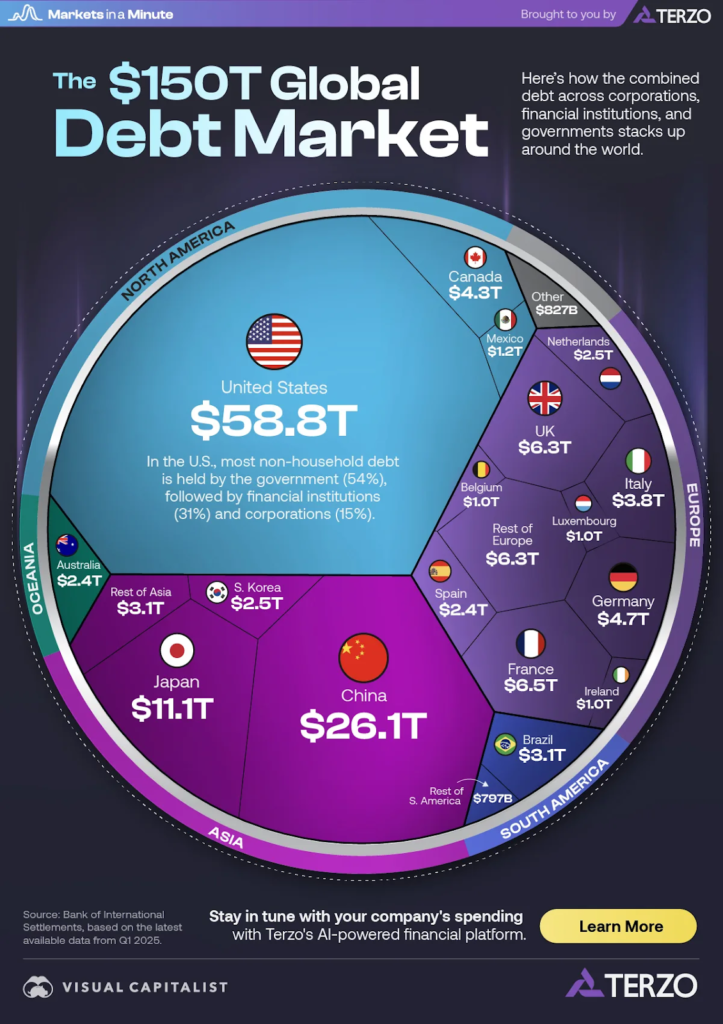

Global debt has hit record highs — crossing $315 trillion according to the Institute of International Finance (IIF). This figure represents over 330% of global GDP, an all-time high.

Much of this explosion in borrowing came after the pandemic, as nations borrowed heavily to stabilize their economies. However, what once seemed like a temporary measure has snowballed into a structural threat.

In 2025, three major debt trends are converging:

- Government borrowing to fund welfare, infrastructure, and defense spending.

- Corporate leverage driven by cheap credit that’s now maturing in a higher-rate environment.

- Consumer debt, including mortgages, credit cards, and student loans, hitting unsustainable levels.

Real-World Example:

Japan’s debt-to-GDP ratio now exceeds 260%, while the U.S. hovers near 125% — levels previously associated with crisis-prone economies. When the largest players in the global economy carry that much leverage, small shifts in interest rates can shake the financial system.

2. How Does Rising Global Debt Affect U.S. Investors?

Many Americans assume foreign debt crises don’t concern them. That’s a costly misconception.

Here’s how global debt indirectly hits U.S. portfolios:

- Dollar Volatility – As other nations struggle to repay dollar-denominated debt, demand for the U.S. dollar spikes, making exports more expensive and pressuring U.S. growth.

- Bond Market Instability – Foreign investors may dump U.S. Treasuries to cover domestic shortfalls, driving yields higher and reducing the value of existing bonds.

- Stock Market Contagion – Debt-driven recessions abroad (like China or the Eurozone) can trigger sell-offs that ripple through U.S. equities.

Case in Point:

In 2022, when Sri Lanka defaulted, it was considered isolated. But by 2024, similar debt pressures emerged in Egypt, Ghana, and Argentina, proving how fast contagion can spread — even to developed markets through bond and trade exposure.

3. Why Inflation Isn’t the Only Wealth Killer

Most financial headlines have focused on inflation as the main economic threat. However, rising debt is a longer-term drag on wealth creation.

Here’s why:

- Inflation can cool down — but debt must be repaid or refinanced.

- Higher debt service costs eat into government budgets, reducing future spending power.

- Central banks may be forced to keep rates lower to avoid mass defaults, fueling asset bubbles.

In short: inflation erodes purchasing power temporarily; debt destroys financial resilience permanently.

4. What Happens If Major Economies Start Defaulting?

Defaults are no longer a “developing country” issue. The IMF warned in early 2025 that over 50 nations are at risk of debt distress.

If large economies such as Italy, Brazil, or China face restructuring, the shock could cascade across the global financial system.

Consequences for Americans may include:

- Stock Market Corrections (particularly in financials and commodities).

- Pension Fund Strains due to foreign bond exposure.

- Reduced Dollar Confidence, if the U.S. government responds with aggressive stimulus.

5. Are Central Banks Making It Worse?

Ironically, yes — and no.

Central banks like the Federal Reserve and European Central Bank have been trying to fight inflation by hiking rates. But these higher rates increase debt-servicing costs for governments and corporations alike.

According to Moody’s Analytics, global interest payments are expected to exceed $10 trillion annually by 2026 — up 40% from pre-pandemic levels.

This means every rate hike tightens the noose further around debt-laden economies.

6. What Can U.S. Investors Do to Protect Their Wealth?

Here’s what smart investors are doing right now:

- Diversifying globally but selectively: Avoiding overexposure to emerging markets with weak debt profiles.

- Holding short-duration bonds: These adjust faster to rate changes and carry less risk than long-term debt.

- Investing in real assets: Gold, commodities, and real estate often hold value when currencies weaken.

- Building liquidity: Having cash reserves for market downturns provides buying power when others are forced to sell.

Practical Tip:

Review your 401(k) or IRA for heavy exposure to international debt-laden ETFs. If over 20% is in emerging markets, you may be overexposed to risk.

7. Could U.S. Debt Become the Next Global Shock?

Absolutely. The U.S. national debt exceeded $35 trillion in 2025, with annual interest payments surpassing defense spending.

This trajectory mirrors pre-crisis patterns seen in other economies. If U.S. debt continues to rise unchecked, Treasury yields could spike, devaluing bonds and triggering broader financial stress.

In short, America’s “safe asset” status could face its first real test in decades.

8. How Does China’s Debt Crisis Add to the Risk?

China’s “hidden local government debt” is estimated at $13 trillion, much of it tied to unprofitable infrastructure projects.

If Chinese defaults accelerate, U.S. investors could face fallout through:

- Reduced global demand.

- Falling corporate profits for U.S. multinationals.

- Increased financial volatility in global credit markets.

Real Example:

The collapse of China’s Evergrande Group in 2023 wiped out billions in investor value — a preview of how corporate debt contagion travels across borders.

9. Could a Global Debt Crisis Trigger a New Recession?

Yes — and signs are emerging.

The World Bank’s 2025 outlook warns that global growth could fall below 2%, the lowest in decades, if current debt trends persist.

Debt overhangs slow productivity, limit government flexibility, and suppress consumer spending. The next global recession may not be triggered by war or oil — but by a credit squeeze.

10. What Can You Do Right Now to Prepare Financially?

Here’s a checklist for financial preparedness:

- ✅ Rebalance your portfolio quarterly.

- ✅ Prioritize assets with low correlation to equities.

- ✅ Pay down personal high-interest debt — it’s the easiest guaranteed return.

- ✅ Build a 12-month emergency fund.

- ✅ Monitor global macro news from reliable sources (e.g., Bloomberg, IMF, BIS).

Preparedness isn’t paranoia — it’s a wealth preservation strategy.

Key Takeaways:

- Global debt levels are rising faster than economic growth, signaling systemic risk.

- The U.S. is not immune — as global markets tighten, American wealth faces indirect pressure.

- Investors should focus on liquidity, quality assets, and risk diversification in 2025.

- The next financial shock may not come from inflation — but from a debt implosion.

10 Trending FAQs

- What is the current level of global debt in 2025?

Over $315 trillion globally, per the IIF. - Why is global debt rising so fast?

Post-pandemic stimulus, defense spending, and higher refinancing costs. - How does global debt affect U.S. investments?

It increases market volatility, raises interest rates, and impacts stock performance. - Could the U.S. default on its debt?

Unlikely in the short term, but political gridlock and fiscal mismanagement raise risks. - What sectors are most exposed to debt crises?

Real estate, banking, and emerging market funds. - Should investors avoid foreign bonds?

Not entirely — but diversify and limit exposure to high-risk regions. - Is gold a good hedge against debt risk?

Historically, yes — gold performs well during currency or credit stress. - Will the global debt bubble burst soon?

It depends on rate policies; however, restructuring pressures are already visible. - What are safe investments during a debt crisis?

Cash equivalents, U.S. Treasuries (short-term), and quality dividend stocks. - How can individuals reduce personal debt risk?

Budget wisely, refinance at lower rates, and avoid variable-rate loans.

Final Thoughts

Global debt is not a distant, abstract number — it’s a ticking economic fuse that could redefine wealth security. For U.S. investors, understanding these dynamics is not just financial literacy — it’s financial survival.

Stay informed, stay diversified, and above all, stay liquid. The next crisis won’t announce itself; it’ll unfold quietly — just like the debt that caused it.